Snapshot

The markets powered higher, with US equities reaching new highs thanks to the stronger-than-expected earnings and the upbeat outlooks of the largest tech companies. Sentiment was also supported by improving odds of the US Federal Reserve (Fed) cutting interest rates as early as September amid weakening economic data and lower-than-expected inflation. Labour data was also supportive, with the US unemployment rate returning to a level last seen in November 2021. The path of least resistance seems to be upwards, with the markets now expecting two rate cuts by the Fed in 2024. The coming earnings season will likely dictate the direction of risk assets, while volatility is expected to pick up in the upcoming months due to the US elections in November. However, it seems that the Fed has successfully engineered a “no landing” scenario, which will likely be cheered on by markets and benefit risk assets.

In Europe, investors breathed a sigh of relief as France avoided the worst-case scenario of Marine Le Pen’s National Rally party winning an absolute majority and gaining direct control in the National Assembly. In a surprise result, the left-wing New Popular Front (NFP) won the most seats, resulting in a hung parliament scenario. This outcome, which implies that there is unlikely to be any extreme outcomes with no party holding an absolute majority, is positive for the country. In the UK, the opposition Labour Party won a huge parliamentary majority in the general election, which was in line with market expectations.

Cross-asset1

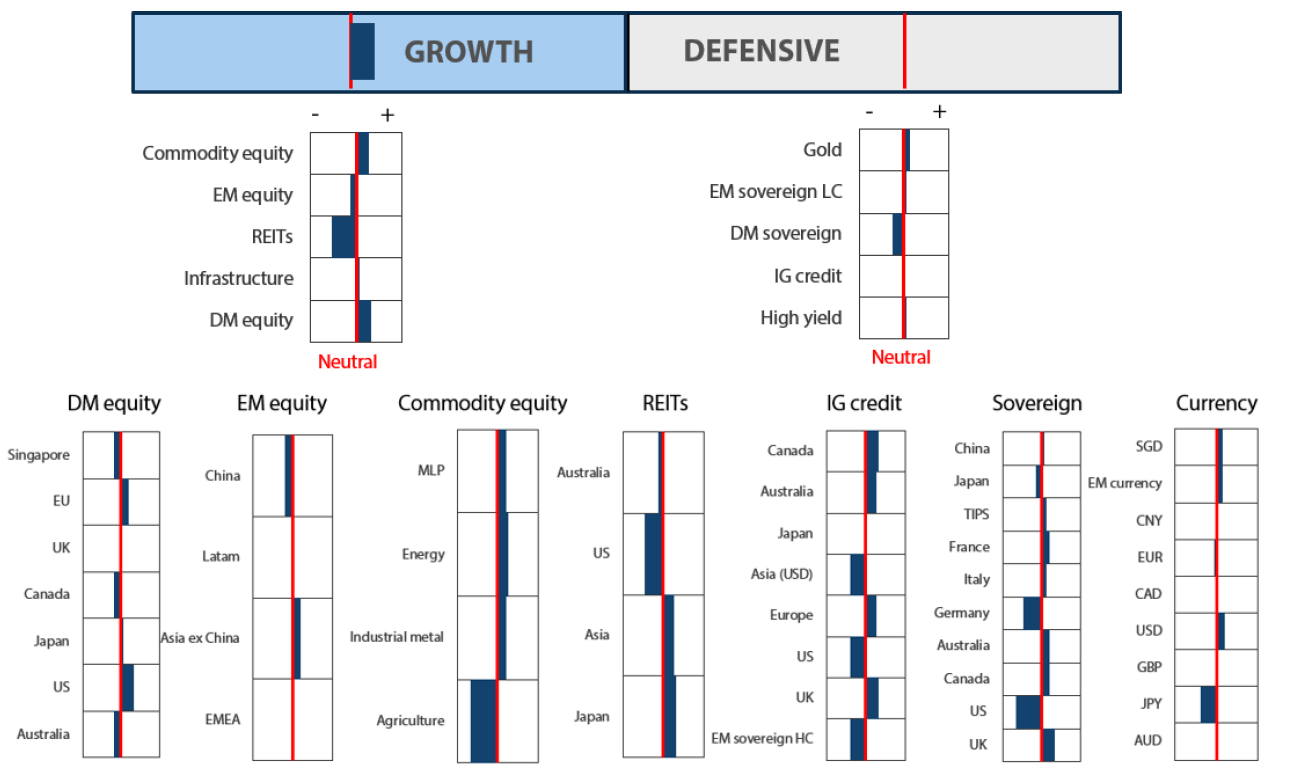

For the month of July, we retained both our overweight to growth assets and our neutral position on defensives. The outlook for growth remains positive as global central banks have started monetary easing, with Europe and Canada leading the way by cutting their interest rates in June. As inflation ebbs globally and economies weaken, there is now more leeway for central banks to cut rates to balance growth. Typically, risk assets do best in an environment when PMIs move from contraction to expansion, supported by accommodative monetary policies. We continue to identify opportunities in a new capex cycle, especially in artificial intelligence (AI) and green initiatives.

Within the growth cross-asset scores, we increased the overweight in developed market (DM) equities by adding to the US, on the back of better visibility driven by secular growth themes. We also added to Europe, given the nascent cyclical opportunities associated with an upturn in global manufacturing. This adjustment was partially offset by reducing the overweight in Japan. We continue to like Japan, but with a slightly reduced emphasis. We also increased infrastructure marginally to reflect our constructive view on the asset class, driven by increasing energy demands due to AI development. We increased our underweight to emerging market (EM) equities due to the better risk rewards found in DM equities despite relative valuation. EM equities continue to be plagued by both structural and cyclical issues, which will take time to resolve.

Within defensives, we marginally reduced investment-grade (IG) credit, bringing it to neutral, while we increased DM sovereigns, though they remain underweight. IG credit spreads remain tight with certain countries (such as the US) trading close to the post-global financial crisis lows. We see relatively more attractive spreads in Canada, where a dovish central bank should support both spreads and outright interest rates. For DM sovereigns, we have a similar preference for Canada and the EU, where we see room for central banks to cut rates, which should be positive. However, due to the highly inverted bond yield curves, we prefer to retain a cautious view on long-dated bonds as the cost of owning them from a hedged yield perspective is relatively high.

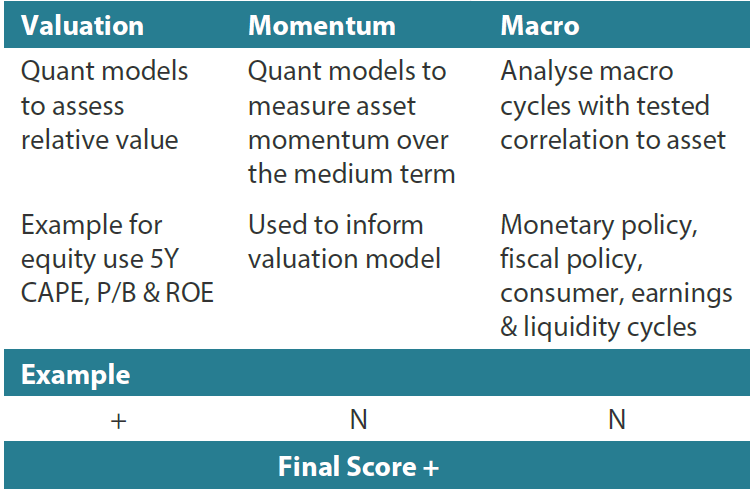

1The Multi Asset team’s cross-asset views are expressed at three different levels: (1) growth versus defensive, (2) cross asset within growth and defensive assets, and (3) relative asset views within each asset class. These levels describe our research and intuition that asset classes behave similarly or disparately in predictable ways, such that cross-asset scoring makes sense and ultimately leads to more deliberate and robust portfolio construction.

Asset Class Hierarchy (Team View2)

2The asset classes or sectors mentioned herein are a reflection of the portfolio manager’s current view of the investment strategies taken on behalf of the portfolio managed. The research framework is divided into 3 levels of analysis. The scores presented reflect the team’s view of each asset relative to others in its asset class. Scores within each asset class will average to neutral, with the exception of Commodity. These comments should not be constituted as an investment research or recommendation advice. Any prediction, projection or forecast on sectors, the economy and/or the market trends is not necessarily indicative of their future state or likely performances.

Research views

Growth assets

Growth assets continued to rally to new highs during the month as sentiment turned to a risk-on mode, fuelled by weaker economic data and easing global inflation. Manufacturing indices are also rebounding from recent lows, suggesting a potential upcycle. Certain sectors, such as tech, which continue to show strong sales and earnings growth, rallied strongly. However, this area is starting to appear somewhat crowded. As such, we seek to find other sources of growth as part of our diversification. One such secular growth theme lately gaining widespread attention is obesity drugs.

GLP-1 and GIP: what are they?

Glucagon-like peptide-1 (GLP-1) and glucose-dependent insulinotropic polypeptide (GIP) are hormones in the gastrointestinal tract responsible for stimulating insulin secretion. Pharmaceutical companies had developed long-acting GLP-1-mimicking drug for diabetes, but they soon discovered that patients were losing weight as their appetite was suppressed. These incretins also slow down gastric emptying, which increases the patient’s sense of fullness. Due to its safety profile and weight-loss efficacy, a higher dose standalone obesity drug was approved by the US Food and Drug Administration (FDA) in 2021.

GIP acts in a similar way to GLP-1 by stimulating metabolism, particularly fat burning. Hence, it was added together with GLP-1, which increased the efficacy of weight loss. The dual-acting obesity drug was finally approved specifically to treat obesity in 2023.

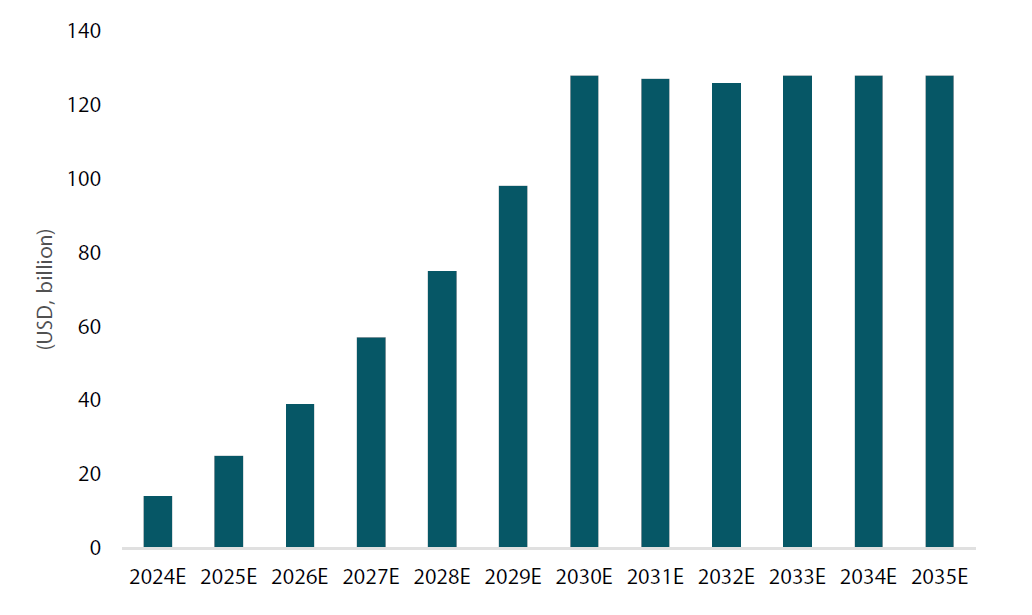

More recently, these drugs were approved by the FDA for the prevention of cardiovascular diseases; ongoing trials aim to show their effectiveness in reducing various diseases such as chronic kidney diseases, apnoea and diabetes. With the approvals by authorities, we believe it would pave the way for insurance coverage and make these drugs available to the general public. The total addressable market size for these drugs is projected to grow from US dollar (USD) 14 billion to USD 128 billion by the turn of the decade.

Chart 1: Estimated global obesity market opportunity

Source: Bloomberg June 2024

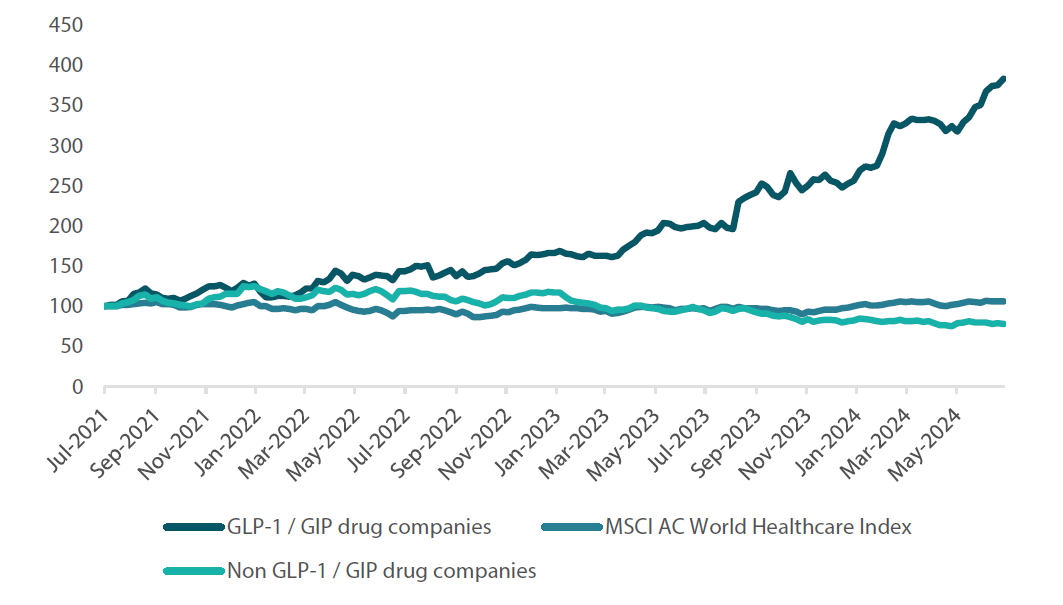

We think that the theme is still in its early stages with significant growth potential ahead. In terms of performance, companies with obesity drugs have done significantly better than those without. When we compare the two largest pharmaceutical companies with obesity drugs with the two largest pharmaceutical companies (by market capitalisation) without obesity drugs, we can see a big difference in performance over time.

Chart 2: Companies with obesity drugs (GLP-1/GIP) versus those without

Rebased to 100 on July 2021

Source: Blomberg July 2024

We think that the incumbent companies will likely face more competition over time. However, the lengthy process of obtaining FDA approvals and the huge capex involved in setting up production should continue to benefit the incumbents as they innovate and evolve their product offerings. For example, they might come up with new methods of administration like oral application and thereby develop moat-like franchises.

Conviction views on growth assets

- Adding to US secular growth: US tech-related stocks continued marching higher as secular and cyclical tailwinds remain strong. Within the US, non-tech stocks lagged the broader rally but we expect them to start catching up as the economy slows and inflation comes under control against the backdrop of a more dovish monetary policy.

- Adding to Europe with elections out of way: We believe Europe provides balance in a portfolio context, offering value and cyclical growth opportunities at still attractive valuations, particularly with anticipated rate cuts. The UK is also seen offering valuation opportunities with rate cuts likely on the horizon.

- Taking some profit in Japan equities: We reduced our overweight to Japan in order to add to the US and Europe, where we see better risk rewards. We are still convinced of the structural reform story in Japan, where we expect companies to start deploying their capital via capex or by returning it to shareholders.

- Still positive on commodity-linked equities: We continue to maintain our overweight position as the asset class continues to provide good diversification opportunities against inflation. The fundamentals of the sector remain compelling due to both cyclical and secular factors.

Defensive assets

Changes within defensive assets were relatively small this month, with adjustments made within Canadian government bonds and European IG credit. Currently the portfolios are positioned to take advantage of rate cuts occurring in Canada and Europe. The two locations have long been viewed as the most likely to move rates first, due to below-trend growth and the rapid pace at which inflation is returning to the targets set by their central banks. This contrasts with the US, where inflation still remains above 3% and growth looks more resilient than expected. While we think that the Fed could adopt a more hawkish stance than the market expects, we also believe that it is preparing for its first rate cut later in 2024. Within the EM local currency positions, we continue to like India due to the continuation of current policies under Indian Prime Minister Narendra Modi’s administration following his election win, as well as a stable Indian rupee.

French elections

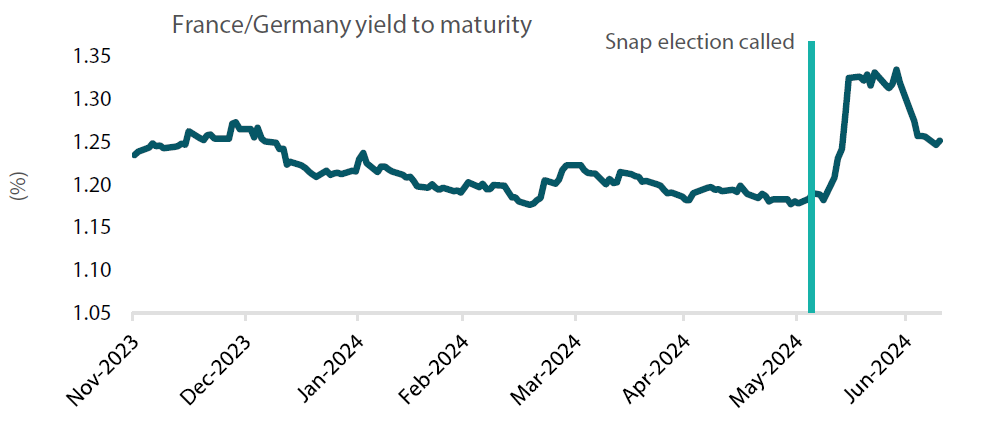

French President Emmanuel Macron took a huge gamble early in June by calling for early parliamentary elections after having suffered a heavy defeat at the European Parliament elections. This spooked the markets, and 10-year French bond yields climbed as much as 12 basis points to 3.28%. Investors were worried about far-right populists taking control of the parliament and pursuing major parts of Le Pen’s expansive fiscal and protectionist “French first” agenda. Since France has one of the larger deficits in Europe, any political party with the power to expand the deficit could be viewed negatively by the market.

Chart 3: French government bond yields spike after Macron calls for snap election

Source: Bloomberg, July 2024

To the surprise of many, the second round of voting for the French elections early in July ended with the left-wing New Popular Front (NFP) party winning the most seats, while Macron’s centrist party won the second largest number of seats and Le Pen’s National Rally party trailing in third.

The NFP party campaigned on left-leaning policies, which include increasing the minimum wage, capping the prices of essential goods and removing the pension reform that increased the retirement age to 64. The party proposed increasing tax rates on businesses to fund the spending, trying to show that the overall cost of their program would be neutral. Given France has one of the larger fiscal deficits in the eurozone at around -5.5% of GDP, the bond market was right to be unnerved about what these policies could represent.

Positively, however, given that it is a hung parliament and each party is almost equally represented, this would mean that it will be difficult for any true legislative change to be pushed through. This will create instability for the French political system. However, it creates more certainty for financial markets, and much like the Indian election result, it may eventually be viewed as a neutral outcome. We would expect the French/German government bond yield spread to continue contracting towards its pre-snap election level; considering the interest rate-cutting cycle that the European Central Bank is entering, we continue to favour French government bonds as a defensive asset within portfolios.

Conviction views on defensive assets

- Short-dated IG credit: Credit spreads remain at fair levels, but many markets still exhibit inverse yield curves, making longer-dated credit less appealing. Until curves steepen, shorter-dated credit is likely to remain our preference.

- Gold remains an attractive hedge: Gold has been resilient in the face of rising real yields and a strong dollar, while proving to be an effective hedge against geopolitical risks and persistent inflation pressures.

- Attractive yields in EM: Real yields in this sector are generally very attractive, and we have a preference for quality EM currencies which can provide strong levels of yield, such as the Indian rupee.

Process

In-house research to understand the key drivers of return: