Snapshot

The strong start to the year for global equity markets hit its first bump in the road in February. While most countries are still delivering a positive return for the year, markets have retreated from their highs to varying degrees. Sharply steeper yield curves have largely been to blame, negatively impacting those markets that benefited most during the height of the pandemic. The technology-heavy NASDAQ index has lost all its 2021 gains after suffering a 10% correction. The broader market indexes that encompass more of the value-oriented “recovery” stocks have performed better.

The interaction between sovereign bonds and equities has been worrisome for multi-asset portfolios so far this year. The role that bonds traditionally play in protecting against equity downside risk has been weakened as higher bond yields are now themselves contributing to the volatility in equity markets. There is a sense of “nowhere to hide”—not so much because yields are rising, but because they are rising sharply. Inflation expectations are also rising rapidly to historically elevated levels as if the economy were already running hot, prompting investor concerns that the US Federal Reserve (Fed) will have to turn the music down and take the punch bowl away.

Of course, the global economy is far from running hot and is still feeling the negative effects of the pandemic. However, more help is on the way as a fresh batch of sizable US stimulus will be unleashed alongside encouraging progress on the rollout of vaccines. Markets are not waiting for hard evidence of a strong economy to position for it—just as markets did not wait for concrete signs of recovery last year to price it ahead of the global economy hitting rock bottom.

So far, the Fed appears to be accepting of higher yields, as indicated by its recent comments that monetary policy is doing its job. In the eyes of the Fed, steeper yield curves and rising inflation expectations are a natural reaction to the impending post-pandemic recovery and reflect investor optimism. On the other hand, it certainly does not want a disorderly repricing in bond markets that has the potential to hurt the real economy. This will be a fine line for the Fed to walk as the recent jump in bond yields has added to equity volatility. However, it may also just be a healthy pause for investors to rotate from pockets of unhealthy froth and rechannel capital to value stocks that should do well in a recovering economy. As reflation takes hold, steeper yield curve pressures will still exist, but as investors move past the initial shock, growth assets will deliver—as they always do—in a growing economy where policy is to remain easy for some time.

Cross-asset1

We have increased our conviction in existing views with a small upgrade to our favourable growth view and a small downgrade to our defensive view. Within growth assets, the increase is predicated on value-oriented equities leading gains in a reflationary environment where real yields are likely to rise. Global yield curves have continued to steepen, with US 10-year bond yields breaching 1.5%, as the US Congress passed a USD 1.9 trillion stimulus package. The rise in bond yields has interrupted global equity gains with prominent selling in growth stocks that benefitted most during the pandemic. Still, given the new fiscal stimulus, the Fed’s commitment to keeping policy easy for an extended period, and the rollout of the vaccine, the outlook for growth assets is quite positive. The recent pull-back in risk appetite is likely to prove healthy given that bullish positioning was overextended.

At the asset class level, we once again nudged up REITs to neutral, which was funded from downgrades to Infrastructure and High Yield as both show lesser upside potential as demand continues to normalise. All other positions remain unchanged, where we still prefer equities and emerging markets in particular. We also favour emerging market (EM) sovereign over alternatives. On the defensive side, we continue to favour inflation assets and investment grade credit over sovereign bonds.

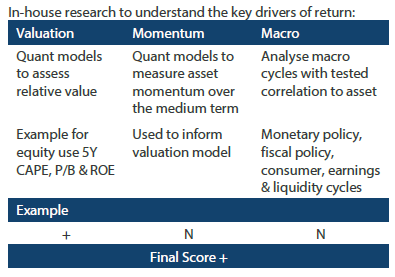

1The Multi Asset team’s cross-asset views are expressed at three different levels: (1) growth versus defensive, (2) cross asset within growth and defensive assets, and (3) relative asset views within each asset class. These levels describe our research and intuition that asset classes behave similarly or disparately in predictable ways, such that cross-asset scoring makes sense and ultimately leads to more deliberate and robust portfolio construction.

1Asset Class Hierarchy (Team View1)")

1The asset classes or sectors mentioned herein are a reflection of the portfolio manager’s current view of the investment strategies taken on behalf of the portfolio managed. The research framework is divided into 3 levels of analysis. The scores presented reflect the team’s view of each asset relative to others in its asset class. Scores within each asset class will average to neutral, with the exception of Commodity. These comments should not be constituted as an investment research or recommendation advice. Any prediction, projection or forecast on sectors, the economy and/or the market trends is not necessarily indicative of their future state or likely performances.

Research views

Growth assets

The equity rotation grew more aggressive in February on the back of a fast-steepening yield curve. While value has outperformed growth for several months now, this month showed more aggressive selling of richly priced securities to scoop up value plays such as financials and energy that have better growth prospects in a more prosperous economic setting.

While the Fed has continued to assure markets that any form of tightening is a long way off, it has also cheered the lift in long-term rates as evidence that its policies are working. Of course, while 10-year yields breaching 1.5% seems a big lift compared to the low of 0.5% set in early August 2020, it is still below the 1.90% level seen at the beginning of 2020, just before the pandemic crisis hit. In other words, policy remains undoubtedly easy, but the repricing of rates does justify a rethink of valuations for the frothiest parts of the equity market.

Some have expected the Fed to announce “operation twist” or some variation to control long-term rates, but it may not need to given ample fiscal stimulus, soon increased by USD 1.9 trillion, on top of a so far successful vaccine rollout. Logically, the Fed does not need to control long-term rates to support growth considering the multiple pillars of growth support, so letting rates run for a bit might just be the right formula for tempering the eventual impact of tapering asset purchases—when the time comes.

Growth assets are still attractive given the positive and still improving growth outlook, but we are cautious on richly priced growth assets that may have further to correct.

Bracing for high growth

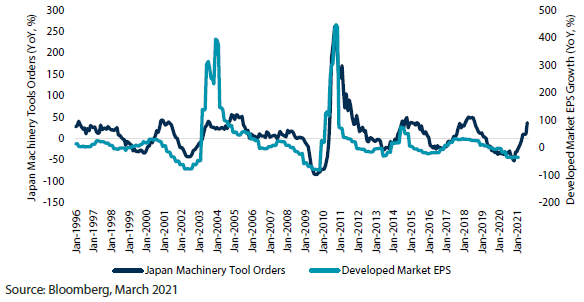

The vaccine rollout is progressing better than most expected, while the full USD 1.9 trillion stimulus passed by the US Senate this past week also exceeded expectations. In fact, the US may just be a quarter away from achieving herd immunity to allow for a full reopening and a likely burst in pent-up demand. Already, the engines of growth are preparing, such as with Japan machinery orders that tend to precede a revival in global earnings.

Chart 1: Japan machinery orders a “canary” for better earnings growth ahead

Manufacturing and earnings have always ebbed and flowed in mini cycles driven by economic and policy shocks followed by easing, while the current cycle is likely to see an explosion of growth not seen in a decade, stemming from the depth of the pandemic shock and the massive stimulus that now waits to feed pent-up demand.

Unlike after the global financial crisis, when growth was hampered by weak banks and an overleveraged consumer, today bank and consumer balance sheets are quite strong and improving due to large amounts of stimulus going directly to the consumer. It is difficult to say how much of these savings will be deployed to meet pent-up demand, but it is safe to say that it is likely to be sizable and probably stronger than any recovery in recent history.

Never have governments been so generous with fiscal stimulus outside of wartime. This is a new era, which the term “reflationary” only partially describes. The Fed stands ready to intentionally let the economy “run hot” to lift the average rate of inflation to 2%, a level which to date has remained stubbornly out of reach. We think the Fed will succeed this time, and we only hope that it will not unanchor inflation expectations in the process.

In any event, earnings growth will be very strong in the coming quarters, making equities a better defensive asset than fixed income where yields have to keep rising—if allowed by central banks.

Conviction views on growth assets

- Lifting REITs to neutral: REITs may still be damaged in particular segments of the market, but the asset class may just be the best “recovery play” given the still-attractive valuations and likely boost to earnings once demand begins to normalise in the summer months. In contrast, we grew more cautious of US High Yield and Infrastructure, which are fully priced.

- Still favouring EM over developed markets: EM experienced some degree of outflows given the recent equity volatility coupled with USD strength. However, we think the bout of dollar strength will dissipate and flows will return as EM remains one of the strongest beneficiaries of returning global growth.

Defensive assets

We downgraded our view on defensive assets from an already negative stance. The steepening trend in global yield curves accelerated in February as momentum turned negative and investors began to contemplate the eventual winding down of central bank support. The rollout of vaccinations in many countries, along with ongoing pandemic fiscal support, points to a rapidly improving global economic outlook. We expect central banks to be patient and believe they are unlikely to withdraw support prematurely, instead waiting until reflation is well entrenched. As a result, strong post-pandemic demand will lead to rising inflationary pressures such that investors will demand greater compensation via higher nominal yields in absorbing the increased sovereign bond supply expected this year.

Investment grade (IG) credit spreads were marginally stronger this month as the sector partially weathered a jump in benchmark yields. Higher yield levels will revive some interest in the short term, but further rises will continue to hold back total returns. Nevertheless, the yield premium offered by IG credit still makes it preferable to sovereigns and we maintain our favourable view relative to sovereign bonds.

Inflation protection assets should also continue to perform well in a reflationary environment, and we maintain our favourable view. Breakeven inflation rates have been on the rise although recent inflation readings are still muted. However, we are looking ahead and expecting higher inflation outcomes. Base effects will boost annual inflation and business’s pricing power will improve as the global economic recovery picks up steam. This is already being reflected in rising expected inflation indicators which will continue to lend support to inflation assets.

Yield curves are on the move

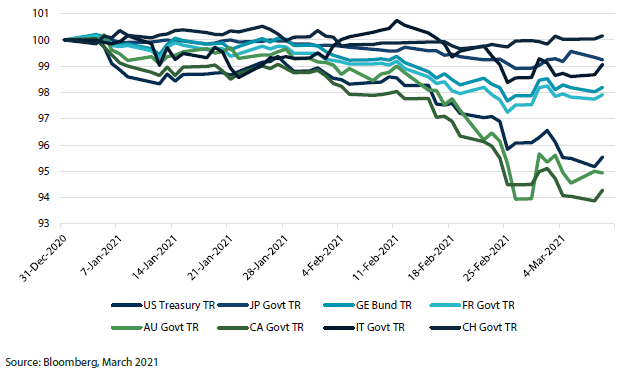

Sovereign bond returns have been disappointing so far in 2021, to put it mildly. Global yields have been trending upwards since October last year, but the rise has accelerated of late, led by longer maturities. The main culprit has been a sharp steepening of the US yield curve which has dragged its dollar-bloc stablemates, Canada and Australia, along for the ride. Core European bonds have done a little better, and investors with sovereign exposures in China, Japan and Italy may have seen mildly positive to mildly negative returns so far. Chart 2 shows the three groupings by total return year to date.

Chart 2: Sovereign bond returns (7- to10-year maturities)

While there are numerous factors at the global level and the individual country level that have contributed to the sharp rise in yields, there is little doubt that investors have been upgrading their global outlooks in expectation of a post-pandemic surge in demand. As a result, all eyes have turned towards central banks for any signs that the extraordinary monetary policy support provided over the last year may be nearing an end. For their part, central banks have so far been steadfast in their forward guidance that rates will stay low for many months to come.

Although this central bank guidance does provide some comfort to bond investors, we also know that yield curves typically reprice well before that guidance changes. Given that most central banks are aiming to reduce quantitative easing (QE) asset purchases before any adjustments to cash rates, this is where our initial focus lies. How investors perceive each central bank’s commitment to its QE policy is one factor that we believe is behind the divergent fortunes of sovereign bond returns.

Our assessment of this commitment to QE, and the resulting reluctance to wind it back, starts with the strongest proponents. We expect the Bank of Japan and the European Central Bank to hold onto QE policies the longest, assuming either bank is ever able to exit. At the other end of the spectrum we would nominate the Reserve Bank of Australia as the least committed to its QE policies, followed by the Bank of Canada and the Bank of England. Occupying the middle ground is the Fed although we would place it closer to the first group given its dovish leanings under current leadership.

These perceptions of how central banks will behave also contributes to how we view current sovereign bond spreads. One example is the UK where we expect the Bank of England to be one of the first to exit QE although its 10-year bond yields trade significantly under US Treasuries where we expect the Fed to hang on for longer. This is perhaps a hangover from the Brexit uncertainty and its struggles with the coronavirus, but caution is definitely warranted if our assessment is correct and the Bank of England is one of the first to retreat from QE policies.

Conviction views on defensive assets

- Long rates will remain under pressure: Rising inflation expectations and increases in forward-looking gauges of price pressures will continue to feed the yield curve steepening trend.

- UK gilts looking particularly expensive: Gilt yields are currently trading significantly under its dollar-bloc peers at a time when the UK’s vaccination programme is proceeding rapidly, and its central bank may prove to be more hawkish than others.

Process