Global equity investment philosophy

Our philosophy is centred on the search for “Future Quality” in a company. Future Quality companies are those that we believe will attain and sustain high returns on investment. ESG considerations are integral to Future Quality investing as good companies make for good investment. The four pillars we use to assess the Future Quality characteristics of an investment are:

Franchise—does the company have a sustainable competitive advantage?

Management—does the company make sound strategic and capital allocation decisions?

Balance Sheet—is growth appropriately financed?

Valuation—are the company’s prospects under-appreciated by the market?

We believe that investing in Future Quality companies will lead to outperformance over the full market cycle. Our strategy is based on fundamental, bottom-up research therefore sector and country allocations are a function of stock selection. The Global Equity strategy is a concentrated, high conviction portfolio with a high active share ratio.

Was the June Federal Reserve meeting a bell-ringing turning point for the economy and the markets?

Equity investors reacted violently to the Federal Reserve's (Fed) June meeting narrative, rotating into IT and growth stocks while selling most of the recent winners – with energy being the exception. The moves were short term, though some of the largest following seven decades of Fed meetings. Investors clearly believed that the economy has become more rate sensitive over time, no doubt because the debt-to-GDP ratio has marched ever higher. However, the US housing cycle, typically the epicentre of rate sensitivity, looks to be resilient with record-low inventories, a 20-year high in the first-time buyer share of activity and still decent affordability.

The outlook for interest rates matters much more today than in the past, because more than a third of the equity market’s capitalization has been moving in sync with the bond market. That cohort includes all SPACs, the FAANG stocks and most of the growth segment. Is it possible that the high growth segment, with limited free cash flow generation or high return profile, might again lead the market higher? Today’s starting point – a 60% PE premium to the market - is high, suggesting the odds are against them.

With such uncertainty, we believe the appropriate approach is to have a balanced portfolio. In addition to strong franchise and management qualities, Future Quality investing coupled with paying close attention to valuation and balance sheet support provides that balance, in our view. The case for balance is strong, given the valuation starting point of the market and the many unknowns such as the sustainability of inflation. Much will be data dependent and making macro calls today may be foolhardy.

Fortunately, we are stock pickers. As uncertainty rises, we dig deeper into the stocks to find answers. There, we continue to find many companies gaining market share, sustainably raising prices and margins, or companies that are restructuring and on a clear path to improving returns, regardless of the macro “noise”. Future Quality provides us with focus when some are losing theirs.

Our valuation discipline remains anchored largely on the one aspect of a company’s financial performance that is the most difficult to produce via accounting creativity - that is cold, hard cashflow generation. More specifically, we want our companies to be able to generate their own investment firepower and sustainably invest this cash, with a high likelihood that the investment will deliver a higher return relative to what the company is enjoying at the time of investment. These investments need to be able to stand the test of time and not see their value quickly undermined by a tougher economic cycle or competitors making similar investments into identical products.

It is this latter point that keeps us underweight in the commodity sectors, though it would be fair to say that we are considering how long the current upcycle in commodities will last; delivering on a future green economy will certainly be difficult, without first investing in a lot of copper and even oil. We continue to believe that companies that solve today’s key social and environmental problems will have the opportunity to deliver strong returns for all stakeholders, including shareholders. Reducing the cost of healthcare provision remains a great example of this and is the core reason behind our long-term overweight in the healthcare sector.

We will continue to act in situations in which share prices become temporarily detached from our assessment of these cash flows and the returns that management teams will be able to realise by investing in them. In recent months, we have continued to take profits in a number of compelling, long-term growth names, whose continued success, in our view, is already reflected in today’s share prices. We continue to find Future Quality opportunities and increase our holdings in companies whose share prices appear to be consolidating before heading higher.

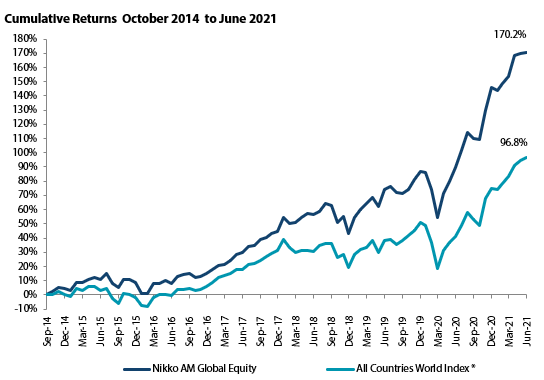

Comparative returns are against the MSCI All Countries World (ex Australia) Index

Global Equity Strategy Composite Performance to Q2 2021

*The benchmark for this composite is MSCI All Countries World Index. The benchmark was the MSCI All Countries World Index ex AU since inception of the composite to 31 March 2016. Inception date for the composite is 01 October 2014. Returns are based on Nikko AM’s (hereafter referred to as the “Firm”) Global Equity Strategy Composite returns. Returns for periods in excess of 1 year are annualised. The Firm claims compliance with the Global Investment Performance Standards (GIPS ®) and has prepared and presented this report in compliance with the GIPS. GIPS® is a registered trademark of CFA Institute. Returns are US Dollar based and are calculated gross of advisory and management fees, custodial fees and withholding taxes, but are net of transaction costs and include reinvestment of dividends and interest. Copyright © MSCI Inc. The copyright and intellectual rights to the index displayed above are the sole property of the index provider. For more details, please contact Nikko Asset Management. Data as of 30 June 2021.

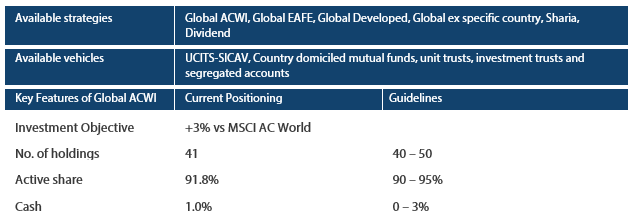

Nikko AM Global Equity: Capability profile and available funds (as at 30 June 2021)

Past performance is not indicative of future performance. This is provided as supplementary information to the performance reports prepared and presented in compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. Nikko AM Representative Global Equity account. Source: Nikko AM, FactSet.

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually “joining the dots” across geographies, sectors and companies, to find the opportunities that others simply don’t see.

Experience

Our five portfolio managers have an average of 24 years’ industry experience and have worked together as a Global Equity team for eight years. Two portfolio analysts, Michael Chen and Ellie Stephenson joined in 2019 and are the first in a new generation of talent on the path to becoming portfolio managers. The team’s deliberate flat structure fosters individual accountability and collective responsibility. It is designed to take advantage of the diversity of backgrounds and areas of specialisation to ensure the team can find the investment opportunities others don’t.

Future Quality

The team’s philosophy is based on the belief that investing in a portfolio of Future Quality companies will lead to outperformance over the long term. They define Future Quality as a business that can attain and sustain high return on investment. We believe that ESG considerations and Future Quality investments are not independent of each other and as such the team evaluate the materiality of ESG factors when assessing the Future Quality potential of each stock.

Execution

Effective execution is essential to fully harness Future Quality ideas in portfolios. We combine a differentiated process with a highly collaborative culture to achieve our goal: high conviction portfolios delivering the best outcome for clients. It is this combination of extensive experience, Future Quality style and effective execution that offers a compelling and differentiated outcome for our clients.

About Nikko Asset Management

With USD 281.8 billion* under management, Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income and Multi-Asset strategies. In addition, our complementary range of passive strategies covers more than 20 indices and includes some of Asia’s largest exchange-traded funds (ETFs).

*Consolidated assets under management and sub-advisory of Nikko Asset Management and its subsidiaries as of 30 June 2021.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the Sub-Fund will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.